The dominant narrative about AI and work sounds confident: certain jobs are disappearing. The research, when you read it carefully, says something more measured, and more useful for business owners trying to plan.

In March 2026, Anthropic published a new framework for measuring AI’s labour market impact. The framework matters for New Zealand businesses because it separates what AI could theoretically do from what it is actually doing in workplaces right now. The gap between those two is large, and so is the opportunity it describes.

What Anthropic actually measured

The researchers, Maxim Massenkoff and Peter McCrory, combined three data sources. First, the O*NET database, which catalogues around 800 US occupations and the tasks that make up each one. Second, Anthropic’s own usage data from millions of Claude conversations, captured in the Anthropic Economic Index. Third, a prior study by Eloundou et al. (2023) that scored each task on whether a large language model could theoretically speed it up.

What’s new in this approach. Most AI-and-jobs research has leaned on theoretical estimates of what AI could do. Anthropic’s measure, which they call observed exposure, tracks what AI is actually doing in work contexts, weighting fully automated implementations more than augmentative ones.

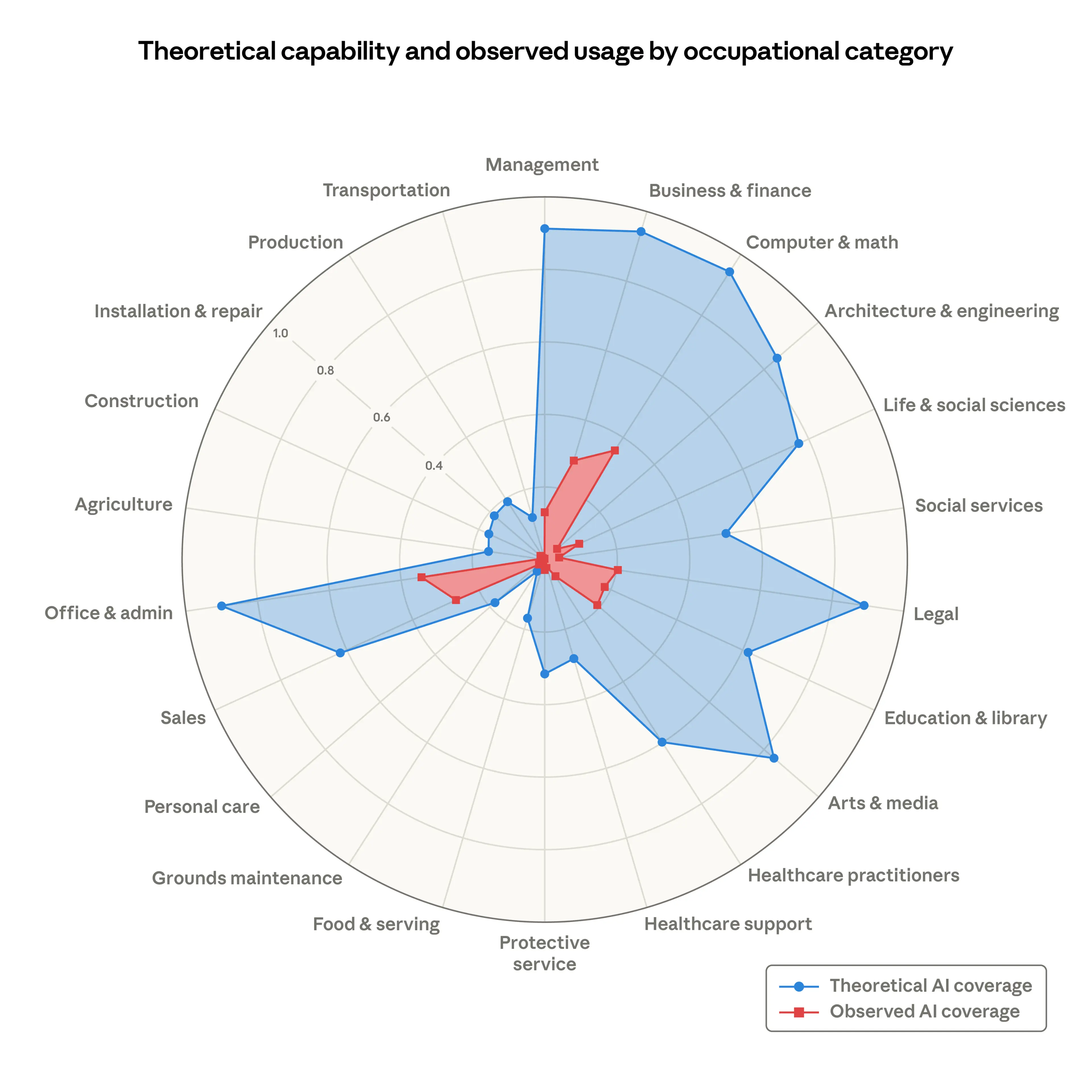

Why that matters. Theoretical capability is a ceiling. Real-world usage is what actually reshapes employment. A task that Claude could perform doesn’t affect a worker until it’s being performed at scale in real workflows. The paper finds that 97% of observed Claude tasks fall in categories rated as theoretically feasible by Eloundou et al., but the share of tasks Claude actually covers within those categories is much smaller. In Computer & Math occupations, the theoretical ceiling is around 94% of tasks; Claude currently covers roughly 33%. That three-to-one gap is the story.

Which work is most exposed today

Exposure is concentrated where you would expect: knowledge work. Computer & Math and Office & Administrative occupations sit at the top on both theoretical capability and observed usage. Business and finance, legal, and educational tasks show significant exposure too. At the other end, physical occupations, agriculture, food preparation, and personal services, show near-zero observed usage of AI.

The pattern is simple enough to state: LLMs handle language. Work that is mostly language, reasoning, and structured information sits in the exposed zone. Work that depends on physical presence, dexterity, or real-world actuation does not.

The specific occupations AI is touching

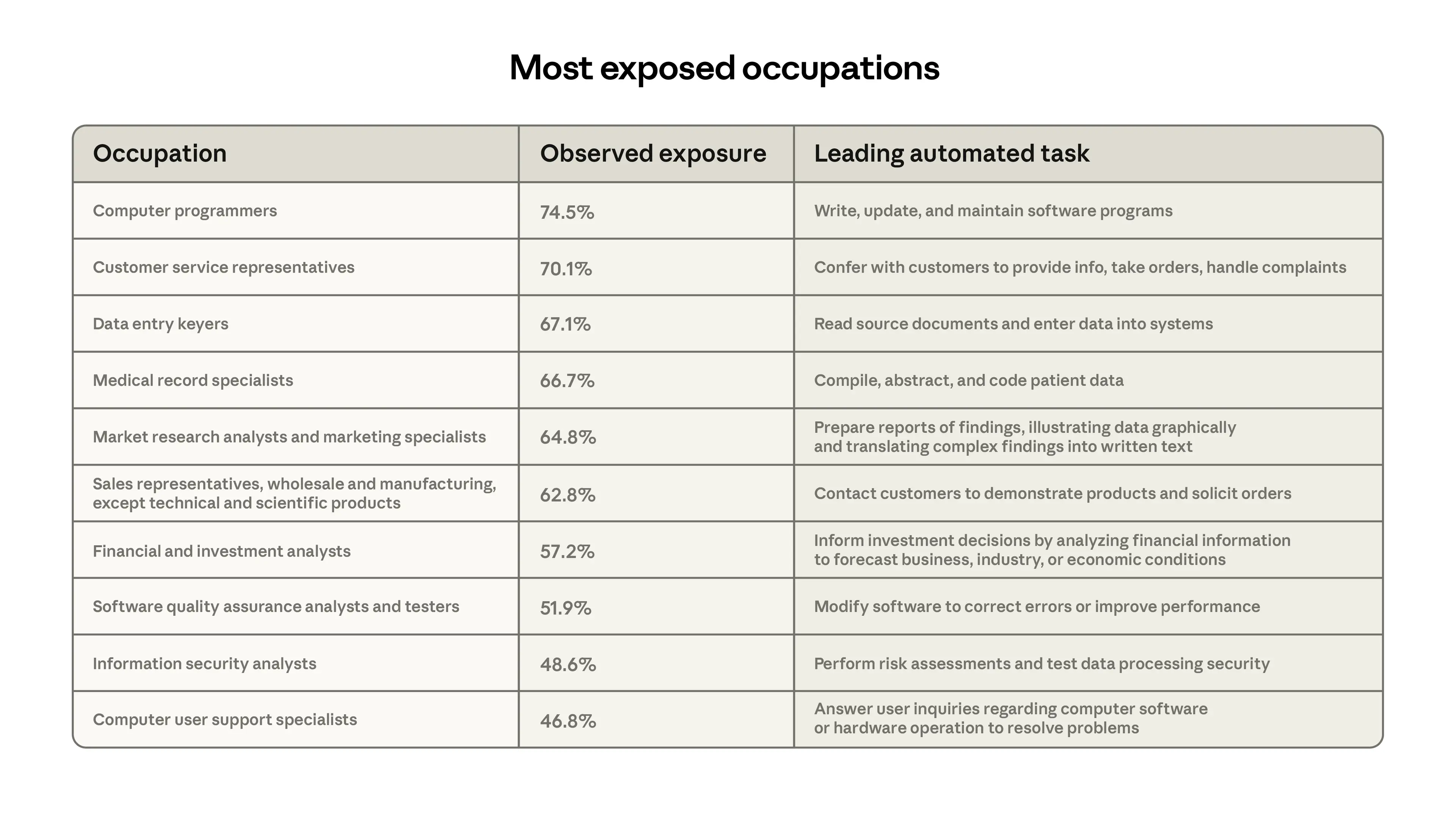

When Anthropic ranks individual occupations by observed exposure, the top of the list is unsurprising but instructive. Computer Programmers lead at 75% task coverage, which lines up with Claude’s heavy use for coding. Customer Service Representatives follow, driven by first-party API traffic. Data Entry Keyers come in at 67%, with document-reading and data-structuring tasks seeing significant automation. Financial analysts and a cluster of related business-analysis roles round out the top tier.

At the other end of the scale, roughly 30% of US workers have zero observed AI exposure in the data. That group includes cooks, motorcycle mechanics, lifeguards, bartenders, dishwashers, and dressing-room attendants. The exposed and unexposed groups look very different demographically too: workers in the most-exposed quartile earn 47% more on average and are almost four times more likely to hold graduate degrees.

The nuance that reshapes the conversation

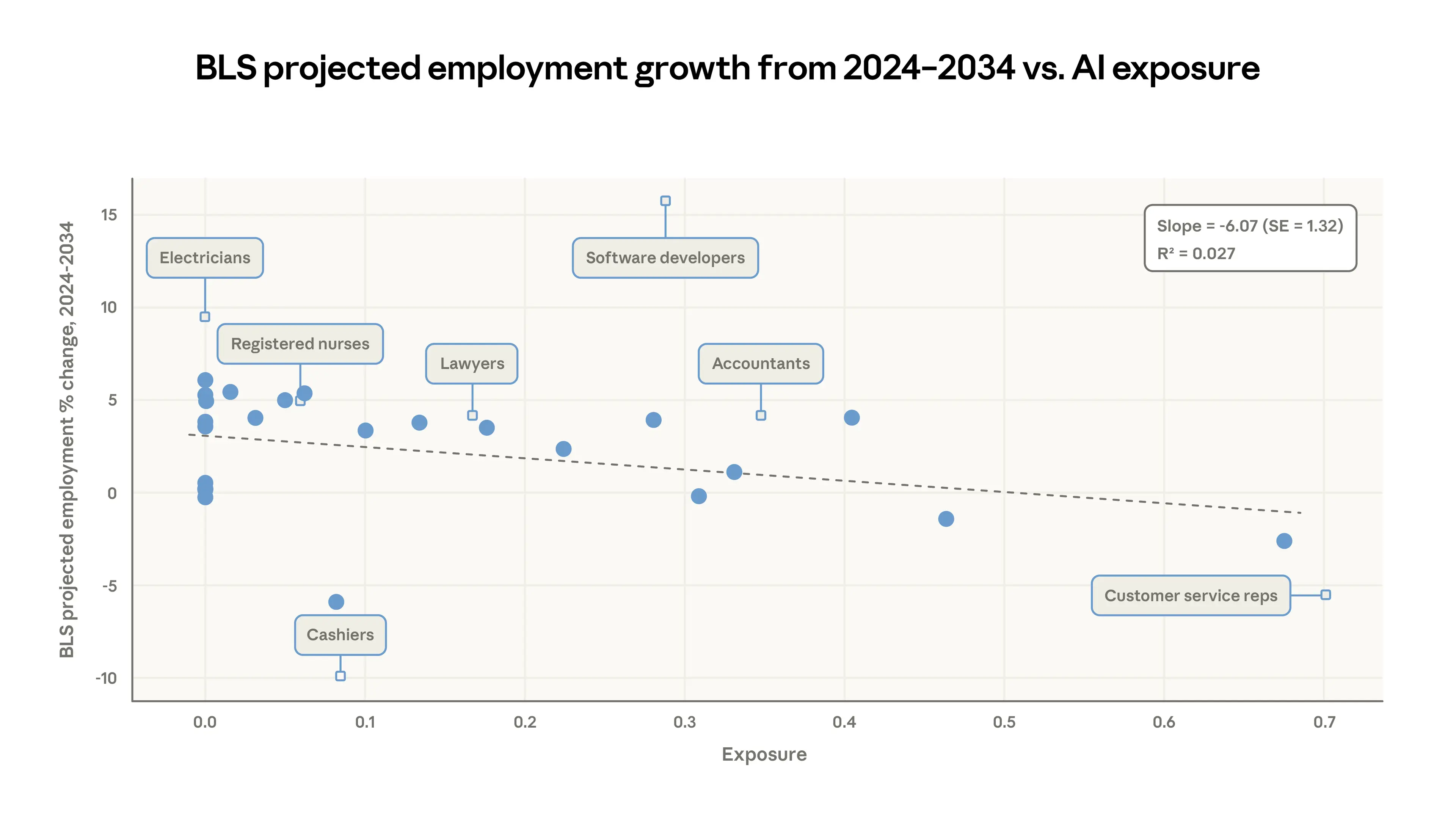

Here is the finding most business owners will miss if they only read headlines. Anthropic found no systematic increase in unemployment for highly exposed workers since ChatGPT’s release in late 2022. Exposure, as the researchers are careful to note, is not the same thing as displacement.

There is one signal worth watching. Job-finding rates for workers aged 22-25 entering high-exposure occupations have fallen roughly 14% in the post-ChatGPT period. This tracks earlier research by Brynjolfsson and colleagues using ADP payroll data. The early effect of AI on the labour market is showing up in hiring patterns for entry-level roles, not in layoffs. The people already doing exposed jobs are, for now, using AI alongside their work. The new workers who would otherwise have joined them are finding fewer openings.

In the language of the paper: on their exposure measure, “fully automated implementations receive full weight, while augmentative use receives half weight.” The fact that exposure is growing without corresponding unemployment suggests augmentation is dominating in practice. That is the single most important framing point for any business thinking about AI and its workforce.

What the data looks like in New Zealand

The US data from Anthropic maps onto the New Zealand economy more directly than most imported research, because New Zealand’s workforce composition sits firmly in the exposed categories. Stats NZ’s most recent GDP figures show business services and knowledge-heavy activity leading quarterly GDP growth, with services broadly accounting for roughly two-thirds of national output.

New Zealand’s adoption numbers tell the same augmentation-dominant story that Anthropic’s exposure data implies. According to the AI Forum NZ’s third productivity report, published August 2025, 87% of New Zealand organisations now use some form of AI, up from 48% in 2023. Knowledge workers report a 84% adoption rate for generative AI, one of the highest in the world.

What is not happening matches Anthropic’s US finding. A Kinetics survey from June 2025 found only 7% of New Zealand businesses reported AI directly replacing workers. In the same dataset, 93% said AI had made their workers more efficient. The AI Forum report records 91% of organisations reporting efficiency improvements, 77% reporting operational cost savings, and 55% saying AI has actively created new career opportunities inside their business. Displacement exists, but it is a minority outcome; augmentation is the majority one.

Where the real gap sits: adoption vs scaling

The 2025 Datacom State of AI Index surfaces the finding that most matters commercially. While 87% of New Zealand organisations use AI in some form, only 12% have scaled it across their entire operations. Another 46% are still running pilots. A further 33% have deployed at the departmental level only. In other words, 88% of organisations have not yet moved AI past partial implementation.

This is the inverse of Anthropic’s 33-versus-94 finding, expressed at the national level. The capability exists. The usage is broad. The full-scale integration is not there yet. Datacom’s report identifies the bottleneck clearly: 32% of organisations cite a lack of internal capability or skills as the main barrier, followed by data quality at 22% and governance uncertainty at 16%. The constraint is not the technology.

The New Zealand Government’s own AI Strategy, released in July 2025, estimates that generative AI could contribute $76 billion to the New Zealand economy by 2038, more than 15% of GDP. That figure is contingent on scaling past pilots, particularly among SMEs, where the AI Strategy separately notes that 68% currently have no plans to evaluate or invest.

What business owners should take from this

The research points to a small set of conclusions that are easier to act on than the usual AI-and-jobs commentary.

- Map tasks, not roles. Both Anthropic’s framework and Datacom’s survey-level view treat work at the task level. Occupations are bundles of tasks, and AI exposure varies within every role. The first useful audit for any business is: which tasks in my organisation fall in the most-exposed categories, and which do not?

- Augmentation is the current state, not a transitional one. The research does not show AI replacing people at scale. It shows AI making people more productive at the tasks they already do. Plans that assume wholesale replacement are planning for an outcome that the data does not support.

- The skills shortage is the real bottleneck. One-third of New Zealand organisations cite internal capability as the primary barrier to scaling AI. Technology and budget barely register by comparison. Workforce capability is the constraint that actually limits value capture.

- Entry-level hiring is the first pattern to shift. Anthropic’s young-worker finding, echoed by Brynjolfsson et al., is a real signal. Businesses that rely heavily on graduate or junior hires in exposed roles should expect the shape of that pipeline to change over the next few years.

- The commercial opportunity is in scaling, not in starting. Most New Zealand businesses already have AI in the door. Very few have moved past pilots. The second phase of AI adoption is about integration and governance, not awareness.

Closing

Anthropic’s paper is explicit that it represents early evidence, and that the framework is designed to be updated as new data arrives. Its central finding, that AI exposure is real but displacement is so far limited, should shape how business owners plan rather than alarm them.

For a business in New Zealand, the practical question is not whether AI will affect your workforce. The adoption data says it already has. The better question is whether your organisation is sitting in the 12% that have scaled it, or the 88% still in pilot. The gap between those two groups is where the productivity, cost, and hiring advantages will compound.

Figuring out what AI adoption looks like in your business?